Staff Working Paper No. 686: Eight centuries of the risk-free rate: bond market reversals from the Venetians to the ‘VaR shock’ - Paul Schmelzing - Bank of England

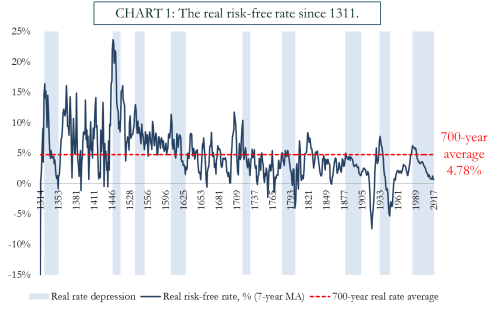

In the midst of historically low interest rates in advanced economies following the Great Financial Crisis and renewed discussions about “secular stagnation” (Hansen, 1939; Summers, 2016), sovereign bond markets have reflected the depressed yield environment and enjoyed years of above-average (price) returns. The current “bull market” in bonds, however, originated prior to 2008 – mirroring the structural dynamics in global inflation rates, which inflected as Paul Volcker’s “war on inflation” triggered by the Oil Shocks started bearing fruit (Goodfriend 1993; Rachel and Smith 2015): it has been recognized that 1981 marked the beginning of a “bull market” period of rising prices and falling yields (Homer and Sylla, 1991), as bond prices typically incorporate investors’ assessment of future inflation and interest rates over the lifetime of the asset (in addition to liquidity, default risk, and term premia considerations, cf. Drake and Fabozzi, 2011).Yet, after 36 years of secularly falling risk-free rates, a significant proportion of sovereign debt recording negative yields, and short-term fallouts such as the 2013 “Taper Tantrum”, more often the enthusiasm in policy and market circles has been giving way in recent years to concerns about an unprecedented “bond bubble” which could eventually inflict significant losses upon holders of government debt. Are such fears warranted? And if we accept the proposition that the bond market shows signs of a “bubble”, how have such conditions normalized in the past? In contrast to the academic references on the history of equity bubbles, the history of bond market reversals remains relatively unexplored territory. This is partly due to a lack of consistent historical data necessary to undertake empirical work in bond markets.

Comments

Post a Comment